Company Insolvency

If your company cannot pay its debts you are likely to find yourself in a frightening and confusing place. This page gives an overview of corporate insolvency (also known as corporate recovery) and explains how we can help you through it.

What is company insolvency?

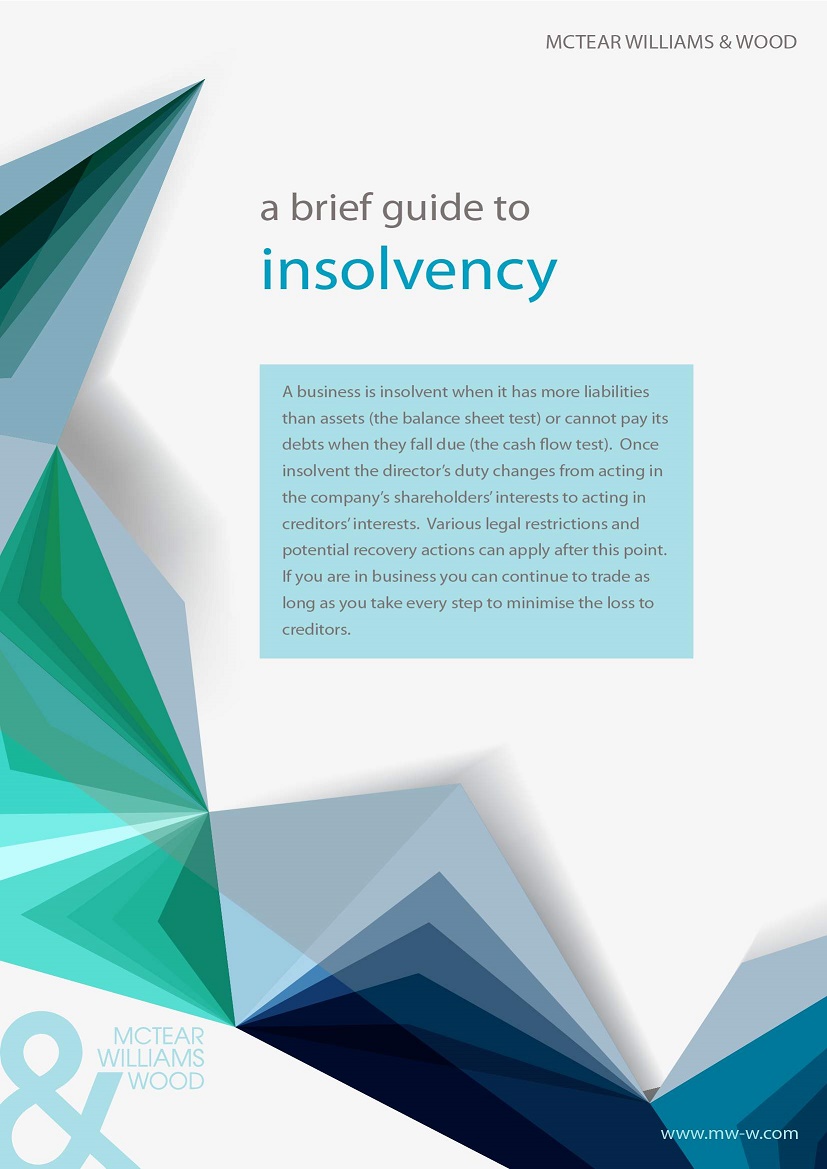

Put simply, company insolvency is when a company has net liabilities, when it has reached the point of no return or cannot pay debts when they fall due it is insolvent. As soon as this happens, directors of the business should take advice from a licensed insolvency practitioner because:

- The situation will impact how the business should be run

- It is sometimes possible to trade out of the situation if advice is sought early enough

- There are strict penalties for 'getting it wrong' that we can help you avoid

How can McTear Williams & Wood help with company insolvency?

If you are a director in this uncomfortable situation you may feel very alone, but we operate in this area the whole time and meet people facing the possibility of company insolvency every day. We promise to help relieve the pressure you're feeling, find the best way forward and give you a clear plan of action.

We deal with more small/medium enterprises (SME) and family businesses in the South East of England than any other firm and so have a deep appreciation of the issues facing owner managers and how best to navigate these. See below for further information on insolvency options, contact our insolvency practitioners for free on 0800 331 7417 or view our Brief Guide to Insolvency.

It is important to be aware, however, that directors of an insolvent company have a legal duty to act in the best interests of creditors and need to be careful to avoid wrongful trading (and personal liability!) or other misconduct which could lead to disqualification. This may sound worrying, but we can assess your situation relatively quickly and give you the guidance you'll need. Our initial meeting with you is free and in confidence. During a discussion with our practitioners we'll talk through all possible options (click on the links below for a fuller explanation), such as:

- Administration

- Administrative receivership

- Pre-pack administration

- Creditors' voluntary liquidation

- Company voluntary arrangement

- Compulsory liquidation

- LPA/fixed charge receiverships

If we can help with any company insolvency queries, we encourage you to get in touch to discuss the next steps. For free initial advice on your situation please call our experts on 0800 331 7417